Building a

'culture of saving'

in rural Colombia

Because banks and credit unions have little presence in rural areas, traveling to a branch to conduct transactions frequently takes time and money many people do not have. A program run by the Colombian government and the World Council of Credit Unions is increasing financial inclusion in rural areas near the Venezuelan border.

Vicky Abreo runs a small convenience store out of the front of her home, selling a little bit of everything to neighbors along her small mountaintop dirt road. This area of the municipality, known as La Cuchilla, is about two hours by bus on winding, partially paved mountain roads from the closest big city, Cúcuta.

A roundtrip from La Chucilla to Cúcuta costs about 60,000 pesos

A roundtrip from La Chucilla to Cúcuta costs about 60,000 pesos

With no way to learn about formal financial services and planning, this distance made it difficult for her to save money and grow her business. But three years ago, she began participating in a savings cooperative in her town. Membership gives her access to additional capital for her store through loans from the credit union, as well as a low-cost savings account.

“Here in our houses we didn’t save, but now that they’ve given us this ability, it’s a very viable thing for us to begin to save,” Abreo said, sitting in the enclosed porch behind her storefront. “And if you have a savings account, you can get a loan.”

"There's no incentive for saving."

Formerly one of many unbanked rural Colombians, Abreo now leads the cooperative group once a month, helping other community members learn about the importance of saving.

“You have more opportunities for your business if you can borrow money,” she said.

Her cooperative is supported by Banca de las Oportunidades, a Colombian government program focused on increasing the number of citizens participating in the financial system, and the World Council of Credit Unions. WOCCU began working in the area in 2016 to increase financial inclusion among rural Colombians in departments that border Venezuela.

The government targeted this region due to the number of Venezuelans fleeing to Colombia in order to offset the stress placed on host communities in areas already struggling with insecurity and lack of economic opportunity.

The program seeks to reach smallholder farmers and other unbanked rural residents, including vulnerable populations such as indigenous people, single mothers, and Colombian returnees from Venezuela.

Savings cooperative members were given piggy banks as prizes at a recent monthly meeting.

Savings cooperative members were given piggy banks as prizes at a recent monthly meeting.

Starting a 'culture of saving'

A main focus of the program is reducing the opportunity cost for accessing savings, loan, and insurance services. Because banks and credit unions have little presence in rural areas, traveling frequently all the way to a branch takes time and money many people do not have.

“We don’t have a culture of saving. We’re just starting. It’s small now, but it’s growing.”

“If they have, let’s say $50, just to travel to the city they spend $10. So there’s no incentive for saving,” said Oscar Guzmán, director of WOCCU programs in Colombia. “The main idea is to reduce dramatically the transactional cost for rural, especially smallholder, households.”

Read: "Coming home," El Salvador’s regional model for return migration.

Colombia is a prime environment for successful financial inclusion programs, Guzmán said, because the country’s regulatory and financial infrastructure is strong enough to support mobile banking, with banks and credit unions widespread in urban areas. Colombian law doesn’t allow cell phone companies to engage in banking transactions, so all mobile services are provided by financial institutions themselves. This means users’ data is very secure because they use the banking systems’ own platforms, according to Guzmán.

With the bank's mobile app, corresponding agents for Bancamia can process transactions and customers can send money to others.

With the bank's mobile app, corresponding agents for Bancamia can process transactions and customers can send money to others.

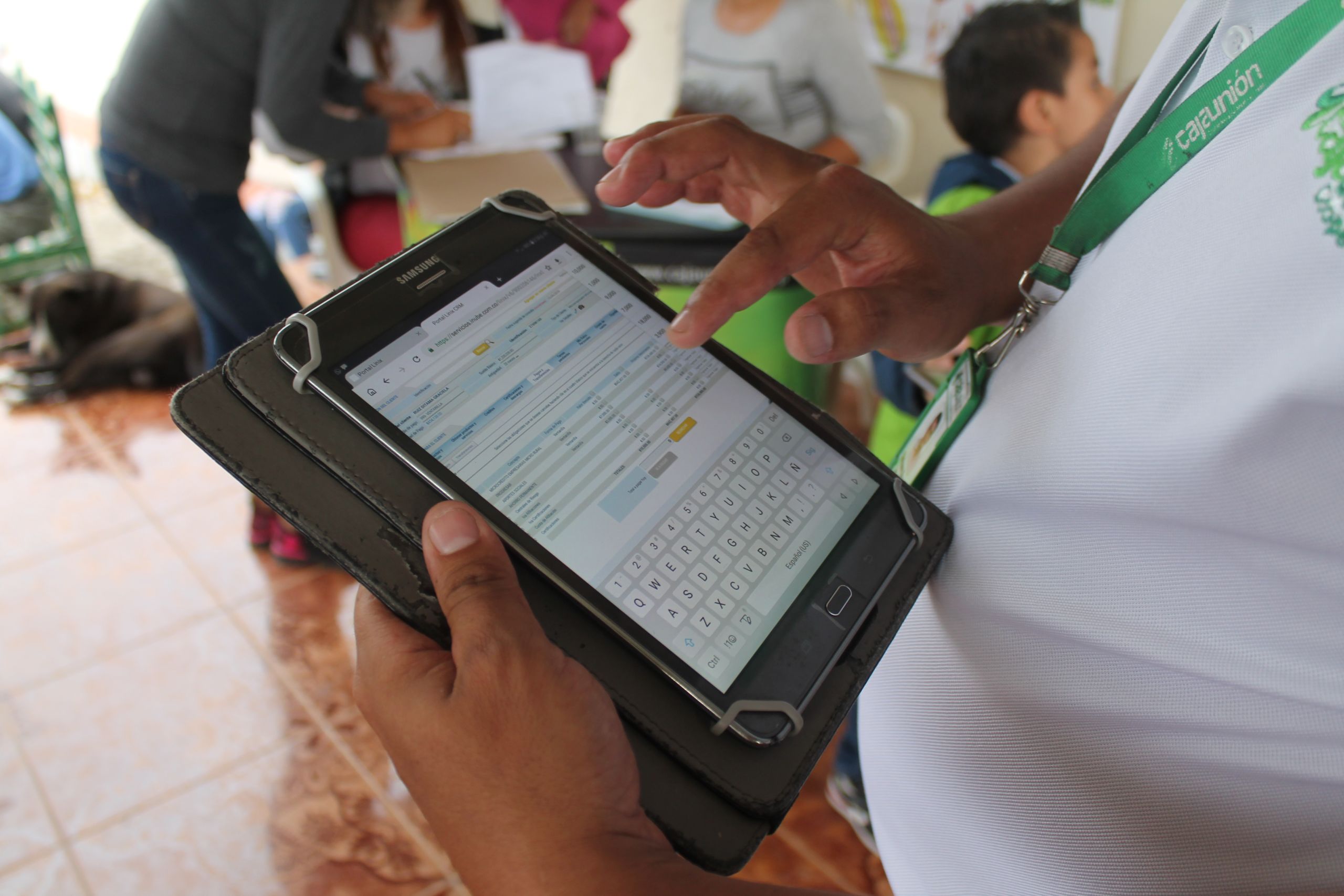

WOCCU has worked with both banks and credit unions to incentivize training and technical assistance to expand services to rural areas, where having a brick and mortar location would not traditionally be lucrative. The organization works with financial institutions to create outposts in smaller towns that are run by staff members of the bank or credit union, as a traditional branch would be. WOCCU also helps create third-party sites called “corresponding agents,” where customers have access to bank products via tablet and smartphone applications.

“What makes it possible? The technology,” said Aldemar Moreno, who runs WOCCU’s programs in the areas surrounding Cúcuta in the Norte de Santander department.

Field agents can use a tablet to process transactions when they have a good internet connection.

Field agents can use a tablet to process transactions when they have a good internet connection.

Diana Carolina Anave is a corresponding agent for Colombian bank Bancamia in Villa del Rosario out of her small electronics shop. She can open accounts, take deposits, and give cash and credit — all from a tablet using the bank’s app. She said there are usually 20 people a day that come to deposit or withdraw cash, with 15-20 people that come for credit services.

Corresponding agents give banks such as Bancamia an opportunity to test the market and grow their customer base in a particular area. Anave’s shop has a red Bancamia sign out front, advertising it as a banking outpost. Anave said that people generally find out about the services by word of mouth and that the community is slowing learning about the benefits of formal banking.

“We don’t have a culture of saving,” Anave said. “We’re just starting. It’s small now, but it’s growing.”

‘Not a peso is missed yet’

Those who live in even more remote areas benefit from savings groups such as Abreo’s, where an 18-person group gathers in La Cuchilla with field officers from credit union Caja Union to process their banking transactions each month.

Members come with the cash they wish to deposit, which can be as little as 20,000 pesos, or about $6. As they hand over their money, it is recorded in ledgers by both the leaders of the savings group and the representative from Caja Union to ensure the amounts are correct. This system allows transactions to be processed in areas where internet connectivity is weak.

Savings cooperative members gather at their monthly meeting where they can deposit funds to their accounts with Caja Union.

Savings cooperative members gather at their monthly meeting where they can deposit funds to their accounts with Caja Union.

The field officer, who is hired from the community, is then responsible for transferring the money back to the branch. Some financial institutions expressed skepticism of a model that sees field officers traveling in remote, and sometimes insecure areas, with a box of cash.

“The bank risk management, the money laundering, the operational areas said, ‘What? You’re going to take money and travel with it? Are you crazy?’ But now they are doing this. Not a peso is missed yet,” Guzmán said.

“We said, ‘It’s the same risk that you have with a cashier in your branch. How many of you have cashiers that stole from you?’ All of them. This is like a cashier. It can happen. But we need to develop the policies and procedures in order to minimize the risk.”

The cooperative, which is about 80% female, also has a program for minors to encourage saving from a young age. Maria Fernanda Ruiztoloza, 15, attended a recent meeting with her aunt. She joined the cooperative last year and wants to become a police officer.

“I’m saving to pay for my career,” Ruiztoloza said.

Joining the cooperative allows members access to credit union services for a discounted rate of 10,000 pesos (about $3) instead of the usual rate — four times that. Potential new members can attend the meetings to learn how the group works without paying the deposit and no commitment.

Retention of current members in the rural cooperatives has been high, said Ángel Castellanos, a coordinator with Caja Union. He said that generally when members want to leave the cooperative, it’s because they need cash for an expense and want to withdraw money. Usually, the group can convince a member to stay by giving them a loan to cover the expense, allowing the member to pay for it without closing their account and stopping their savings plan.

Financial literacy is also a key piece of programming in areas where many people have had little to no interaction with formal financial institutions. WOCCU supports programs that educate people on the importance of saving, how it can help achieve their goals, and how a relationship with a bank or credit union could give them access to funds in the form of loans or microcredit.

"The real challenge is to maintain people saving."

“It’s easy to open an account. We talk to the people and we convince them that savings is important and they open an account,” Guzmán said. “But the real challenge is to maintain people saving. So financial literacy with the financial services together, the result is to have very high rates of use of savings.”

Guzmán said that about 45% of the Colombian population nationwide saves, but participants in WOCCU programs continue saving at a rate of 90-95%. WOCCU’s original goal when the program began in 2016 was to reach 210,000 Colombian adults, something it achieved eight months early. As of early March, the programming has reached 224,378 low-income Colombians with financial services.

Tracking progress, Guzmán said, is important because it demonstrates that the programs can be scaled. And that is key to showing financial institutions that expanding operations to rural areas and the previously unbanked is safe, secure, and good for business.

“One of our main challenges here was … to show them that there is a need but also that there is sustainability, a business case for them to stay in these areas. But not only to maintain [operations] in these areas, but to expand to other municipalities here because we teach them how to manage the risks,” Guzmán said.

“If you don’t show them that this can be done with a minimum risk and in a profitable way, they are not going to scale it.”

Ángel Castellanos explains how the cooperative works to potential new members.

Ángel Castellanos explains how the cooperative works to potential new members.

The view of the surrounding valley from La Cuchilla.

The view of the surrounding valley from La Cuchilla.

Words and photos: Teresa Welsh

Production: Delia Behr

Map graphic: Mariane Samson